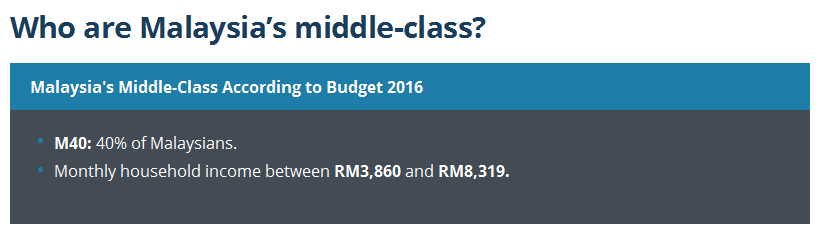

This article is refer from imoney.my, written by Fiona Ho Its a very useful guideline for those who want to climb above and don't want to be left behind in the social chart. I personally don't agree on the categorization of middle class as I think its somewhere around RM3,000-RM10,000 due to inflation and also more high income earner arising. In city or township the range could be even higher as the daily expenses is much higher. Anyhow, the first thing is how to increase your income and at least not left behind? Here's some guideline. Enjoy your learning... Budget 2016: What Can The Middle Class REALLY Do About It? Written by Fiona Ho Last week, Prime Minister Datuk Seri Najib Tun Razak announced Malaysia’s annual budget with the theme, “Prospering the Rakyat.” This year’s affair highlighted the government’s plans to narrow its budget deficit, as well as measures to address issues such as the rising cost of living and housing unaffordability. These measures include increasing its cash handouts under the 1Malaysia People’s Aid (BR1M) assistance programme and raising the minimum wage for workers. They also introduced new income tax provisions, such as the introduction of tax relief for children who provide for their parents and an increase in tax relief from RM1,000 to RM2,000 for each child from year of assessment 2016. But let’s face it – amid inflation woes triggered by the sharp drop in the Ringgit, the introduction of the Goods and Services Tax (GST), and the recent increase in toll rates across the Klang Valley – these measures really don’t do much for those already grappling with the rising cost of living. Middle-income earners who are not eligible for cash aids, and yet do not earn enough to weather the rising living costs, continue to bear the biggest brunt of the current economic situation.  Many middle-income earners in Malaysia are already resorting to drastically cutting back on their expenses, including fewer trips to restaurants to tackle rising living costs.

A better solution for this would be to boost their disposable income. The million dollar question is, how? 1. Generate your passive incomeOne of the easiest ways to do this is by increasing your passive income. Unlike active income (which you usually earn through having a job or running a (profitable) business), passive income generation typically requires less time and effort. Passive income can include investments, especially with low-to-mid risk instruments that let you leverage on capital with minimal active input. This could be in the form of unit trusts, REITs, shares, investment-linked policies or even in your good ol’ fixed deposit account. They let you accumulate returns while you grow your savings pool. The more you save, the more returns you will get. Lower-risk financial instruments like fixed deposit will give you lower returns, but they are generally considered safe and are an effective tool to help preserve the value of your contingency funds. 2. Make your money work harder for youStretch your Ringgit further by adopting strategies that allow you to save while you spend. For example, buying essential items such as rice and toiletries in bulk can save you a small fortune. You can also save a few bucks with hypermarket loyalty cards. Benefits often include reward points, special member price for selected items or additional discounts from selected merchants. They may also offer shopping-related benefits. For example, the AEON member card offers free parking for the first two hours. You can also save money on purchases when you shop at online stores, or by using a shopping credit card that offers rebates or privileges when you shop online. For instance, the CIMB Cash Rebate Platinum card gives you 5% cash rebate and up to 25% discounts when you shop online. Bogged down by fluctuating petrol prices? You can fuel up your purchasing power as you fill up your tank when you use a petrol credit card that gives you cashbacks or reward points. 3. Avoid investment mistakesThere’s a difference between investing and investing properly. Anyone can put their money into investment products, but without a sound financial plan, you may not know which investment strategy or products will work best for you, and how to build a balance portfolio. The key to building your financial strategy starts with understanding your goals and risk appetite. Younger investors typically have a higher tolerance for risk and can afford to make riskier investments due to their longer investment horizon. They also have longer time to work on achieving their financial goals. Next, you will need to identify your short and long-term goals, and how much you can afford to set aside, in order to determine the type of financial products that will work best for you. Without taking these factors into consideration, you may end up investing too much in the “wrong products”, or end up putting all your eggs in the same basket, financial advisor and coach Yap Ming Hui explains on his website. For example, investing in property is not a bad thing. But if you’re putting your entire fortune into a single asset class, you risk “over investing” and exposing yourself to “too much risk”. “If the property sector takes a dip, it will badly affect your investment. In addition, it may also affect your cash flow if you take too much loan to finance your property investment,” Yap says. Having a diversified investment portfolio that comprises various asset classes can help protect your capital from adverse market conditions. 4. Get a financial plannerIf you have the capital and a goal but are a little sceptical on how to reach it, a financial planner can give you a nudge in the right direction and help devise a financial strategy to help you get there. This strategy will work as a road map towards your money goals – whether it is buying a house, saving for your kid’s education, or achieving early retirement. A financial planner can also help you buy or sell, and manage your investment portfolio on your behalf, depending on the nature of the agreement. Some planners do not charge a fee but are paid commissions on the financial products you purchase. Meanwhile, others may charge an hourly rate or a retainer fee. With their expertise, a financial planner can point you to the right financial tools to help you make informed money decisions. The current economic situation is unlikely to improve in the months and years ahead. For the time being, Malaysians will just have to suck it up and learn to adjust to higher prices. While you can’t control the economy, do keep your chin up and focus on what you can control – they lie in the choices that you make every day that can determine your financial future.

0 Comments

Leave a Reply. |

MPIG NewsIn this section we will be sharing on articles & news update related real estate and some other interesting topics. Archives

August 2023

Categories |

- Home

-

New Property Launch

- Lake City @ KL North NEW PHASE FROM RM380k

- Alora Residences – Inspired living within greenery in Subang Jaya

- PJ Spacious and Affordable 5 Star Condo

- Best Investment 2022 PJ Damansara Low Risk Low Entry Price High ROI

- 2022 PJ Rumah Mampu Milik RM270k Damansara

- Bangsar South 2 Rooms from RM390k BELOW Market Price

- 10% ROI PJ Project near Ikea and One Utama Mall

- Mid Valley Seputeh New Launch

- Pavilion Damansara Heights 柏威年 白沙罗岭 马来西亚 吉隆坡 精选楼盘

- 马来西亚RM300千的PJ屋子-首购族,年轻人月入3千能买房

- 2021 Penang Most Awaited Project

- 2021 New Launch - KL Metropolis

- Freehold LRT Linked 3 Room Suites in Glenmarie

- New SPACIOUS Kepong Landed 6 Room 6 Bath

- Bangsar Last Piece Land New Launch

- Avara Seputeh (Mid Valley)

- Project Announcement Registration. Malaysia New Property Launch

-

Existing & Past Project

- 2020 Lowest Risk & Price in Klang Valley with Great ROI

- Kiara East Suite Dex

- 2019 SAFEST PROFITABLE HIGH CASHBACK INVESTMENT

- Best Property Investment Projects in 2018

- KL City Freehold Spacious Affordable 3 room Project

- Jalan Kuching Freehold New Office & Shoplot

- Jalan Ipoh New Freehold Shoplot & Offices

- RM300k KL Sentral New Prelaunch

- The Olive Condo, Sunsuria City

- Prelaunch Landed House Bukit Rahman Putra

- RM260k No Downpayment Puchong South Suites

- PJ North RM400k High Cash Back Project

- Denai Sutera @ Alam Sutera, Bukit Jalil

- First Phase of Banting New Township

- Neu Suites 3rdNVenue @ Embassy Row by Titijaya & CREC

- COURT 28, Jalan Ipoh KL City New Property Launch Service Apartment. Malaysia New Property Launch

- Semanja Kajang New FREEHOLD Kajang Double Storey Houses. Malaysia New Property Launch

- M Suite @ Desa Park North

- BIJI LIVING @ Sek 17 PJ City by Conlay. Malaysia New Property Launch

- Amani Residence Bandar Puteri Puchong New Freehold Service Apartment. Malaysia New Property Launch

- SFERA RESIDENCY @ Puchong South. Malaysia New Property Launch

- KL North Last Release

- PreLaunch Freehold Double Storey

- LAND

- News & Articles

- Other Reference Link & Services

- Referral

- Career

- MPIG

- Get Professional Advice

- PJ八打灵2021全新地产项目分析手册

RSS Feed

RSS Feed